![]()

Free Consultation

Toll Free: 866-432-7093

Representing individuals, businesses, condo associations and homeowner’s associations in a wide range of claims.

Previous

Next

Serving Central, North East Florida

Over

20

Years

Insurance

Assurance Inc.

“Your Public Adjuster”

Claim Reporting avoid Insurance Low Ball, Insurance Low Balling, Claim Denial (2020)

What is a Public Adjuster?

Public Adjusters are your insurance claim adjuster working only for you the insured. The insurance claim adjuster sent by the Insurance Company is their insurance adjuster and has a fiduciary duty to their client the Insurance Company, not you. As your insurance claim adjuster; we inspect the loss site, analyze the damages, assemble claim support data, review the insurance coverage’s, determine current replacement costs, etc. We know how to properly investigate, document and get claims resolved with the maximum recovery.

Be Very Careful of Public Adjusters That come Knocking on your Door After a Devastating Event.

PAST CLAIM EXAMPLES

| INSURER’S ESTIMATE | OUR COLLECTIONS | DIFFERENCE | % INCREASE | STATUS |

|---|---|---|---|---|

| $40,753.74 | $178,802.57 | $138,048.83 | Over 339% | PAID |

| $25,434.27 | $130,670.29 | $105,236.02 | Over 414% | PAID |

| $23,850.00 | $285,262.35 | $261,412.35 | Over 1,095% | PAID |

| $36,244.43 | $181,964.90 | $145,720.47 | Over 402% | PAID |

| $22,199.27 | $99,199.70 | $77,000.43 | Over 347% | PAID |

| $11,215.49 | $486,602.87 | $475,387.38 | Over 4,239% | PAID |

| $3,559.62 | $31,784.41 | $28,224.79 | Over 793% | PAID |

Note: These are average cases. NOT EXCEPTIONS!

Denials Don’t Scare Us!!!

Type of Claim : Business (Restaurant/Convenience Store) – Fire/Smoke

Location : Orlando, Florida

Insurance Company denied claim in its entirety. We documented damage and under appraisal clause of the policy recovered $125,000 for the insured.

Type of Claim : Church – Wind/Water

Location : Pensacola, Florida

The church suffered water damages to the parsonage and Sunday school building. The Insurance Company denied the claim in its entirety. Recovery was $85,000 for the covered damages.

| INSURER’S ESTIMATE | OUR COLLECTIONS | STATUS |

|---|---|---|

| Denied | $27,629.92 | PAID |

| Denied | $81,682.27 | PAID |

| Denied | $184,670.00 | PAID |

| Denied | $329,186.76 | PAID |

| Denied | $2,300,000.00 | PAID |

Typically our collections are 100’s % higher than the Insurance Company’s original estimate. Call today for a FREE consultation. If we inspect your loss and if our investigation finds the Insurers offer fair, you at least have the peace of mind of having a free professional second opinion.

Why should I use Insurance Assurance Inc. Public Adjuster in Florida?

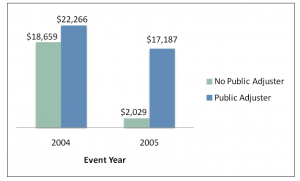

Public Adjuster Representation in Citizens Property Insurance Corporation Claims Extends the Time to Reach a Settlement and Also Increases Payments to Citizens’ Policyholders

Report 10-06, January 2010 https://oppaga.fl.gov/Products/ReportDetail?rn=10-06

Report Summary: The number of licensed public adjusters in Florida has grown significantly in the last six years, and the incidence of complaints, regulatory actions, and allegations of fraud involving public adjusters is generally low. Florida’s public adjuster laws are comparable to and in some cases more restrictive than those of other similar states.

All Public Adjusters Are NOT Created Equally

Hail Damage: After we gained recovery on surrounding homes another Public Adjuster received Denial and gained no recovery for our Clients Neighbor his client.

Recently we had the privilege of handling several Hail claims in a subdivision. While we had successfully gained recovery on surrounding residences another Public Adjusting Firm failed to make recovery, receiving a Denial and the Homeowner gained no recovery.

Hurricane Damage: Public Adjuster Documents Claim for over $800,000 then signs Appraisal Award for less then $100,000

A Large Public Adjusting Firm had made claim over $800.000 in damages in a commercial Claim, although then agreed and signed an Appraisal Award for less than $100,000. When the Insured sued them they were not able to receive recovery as this firm had no Errors or Omissions Insurance. Rather changed their name to a similar one and went back to business as normal.

When Don’t You Need a Public Adjuster?

When they can’t tell you roughly what the damages are and what he will get you paid for?

When they can’t tell the restoration standards for your given loss and assure you that collection will be made in accordance?

When they tell you their estimator will take good care of you;

When they can’t tell you what triggers they will use to settle;

- When you simply don’t wish to deal with the claim yourself

- When the claim is too complicated or large.

- When the insurance company tenders their offer or makes payment get a second opinion from a Public Adjuster It is FREE.

- When the carrier is delaying or Denying your claim. If that adjuster can clearly tell you what he is going to do

Report Your Claim Properly and You may Never Need Professional Assistance.

How to make Insurance Claim?

Do I Have A Claim?

Policies have specific coverage’s and exclusions, Review your policy Coverage’s and Exclusions Read the endorsements and changes, to see how they apply to your claim. If you are unsure if a claim is covered under your policy, call us for free advice.

Note Water Damages; Pipe Breaks, washing machine overflow, Burst Water heater, Shower pan failures, Faulty drain pipes, HVAC Backup, Burst Ice maker lines & appliance Leaks etc. Many policies have exclusion similar to the following prompt reporting is necessary.

“We do not insure for loss caused directly or indirectly by: Constant or repeated seepage or leakage of water or steam, or the presence or condensation of humidity, moisture or vapor; which occurs over a period of 14 or more days”.

Reporting a Claim

*Read your Policy including all Forms and Endorsements*

How the claim is reported can have serious consequence on your claim, the speed of settlement, amount of recovery or your claim could be denied entirely. It is your responsibility to report the claim and the insurance company’s responsibility to investigate the claim you reported.

Some very important pointers;

Don’t limit your claim! Perform a complete and thorough investigation of all property or have a professional investigate the damages so that your claim can properly be reported. We are continually advised damage is confined to one room or area and our investigation finds just as much or even more damage in an adjacent room or area as no one had looked.

Be very careful in explaining the damages and your expectations; an example would be the adjuster asks is there any damage to the furniture, your reply is “see the damage on that table leg”. A few weeks later you receive the adjusters’ summary and it contains $50 to refinish the table’s leg. Can the table leg even be refinished?

The proper way to make claim on this table;

- Is the table part of a pair or set such a dining set? If so advise that the Table is part of set and you are making claim for the set.

- Contact the store of purchase or a reputable furniture refinisher and see if a repair can be done. Advise the contractor of your requirements i.e. to match and restore if the entire set to its condition prior to the loss, refinishers rarely can guarantee total restoration without refinishing the entire set and may not even be able to restore in even attempting the set.

Be very careful of your wording when making claim as words can have specific definition in accordance with the policy.

Flood, by policy definition in many insurance policies is rising ground water and not covered under an ordinary Homeowners Policy. We have seen many claims wrongfully denied just because the ponding occurred due to a covered loss which is covered under the policy, but the claim was reported as a flood and therefore denied.

Report the claim to your Insurance Company and/or your agent. The declaration page of your policy and/or the policy itself provides information for making a claim. Some policies require claim to be made directly to the Insurance Company and not the agent. It is your job to report the claim. It is the Adjuster job to investigate the claim “You Report”.

About Us

Your premier Florida Public Insurance Adjuster successfully representing many policy-holders throughout Duval, St. Johns Clay, Nassau and Flagler Counties. We are Florida residents Serving Central North East Florida since 1999.

INSURANCE PAYS…

WE ASSURE IT!!!

Florida Public Insurance Adjuster Services

Insurance Assurance Inc., your premier Public Insurance Adjuster can offer you variety of different services:

- Public Adjusting Services

- Appraisal Services

- Mediation Services

Commercial/Business Claims

Condominium/Association/Apartment Claims

Residential / Homeowner Claims

Testimonials

” Insurance Assurance, Inc. was one of the best decisions we made after our home owners insurance low balled us on damages. This company went above and beyond to make sure we were treated fairly. Insurance Assurance not only got us results but took the time to walk us through. When the process was complete we had a meeting and were told to call with any questions we may have while doing our repairs. This company not only cares about their clients during the process but also offers their assistance til your back to normal living. I cannot praise this company enough!”

Kim B.

“Insurance Assurance, Inc. got me a good settlement. They are really helpful and take time to guide me through from the beginning (at that time I don’t even have to pay them a dime) I am very happy with their services. If you are looking for a public adjuster that will fight for you, Insurance Assurance is who I recommend..”

Supansa P.

“Insurance Assurance, Inc. has been FANTASTIC. Very easy to work with, I have used a public Adjustor in the past and only wish I had known about insurance assurance!! I have prompt return calls and emails. This team is very knowledgeable and takes the time to explain the process thoroughly!”

Jennifer N.

CONTACT US

- Phone: (321) 735-6428

- Toll Free: 866-432-7093

- Fax: (321) 735-0266

- Email: insuranceassurance@hotmail.com

- License No.: D032331